with Embassy REIT Today and Take Part in India’s Growing Office Real Estate Market!

Embassy REIT is India’s first listed REIT and the largest office REIT in Asia by area. It owns and operates a commercial office portfolio across 5 major cities in India.

Total Area

Office Parks

Gateway Cities

Blue Chip Occupiers

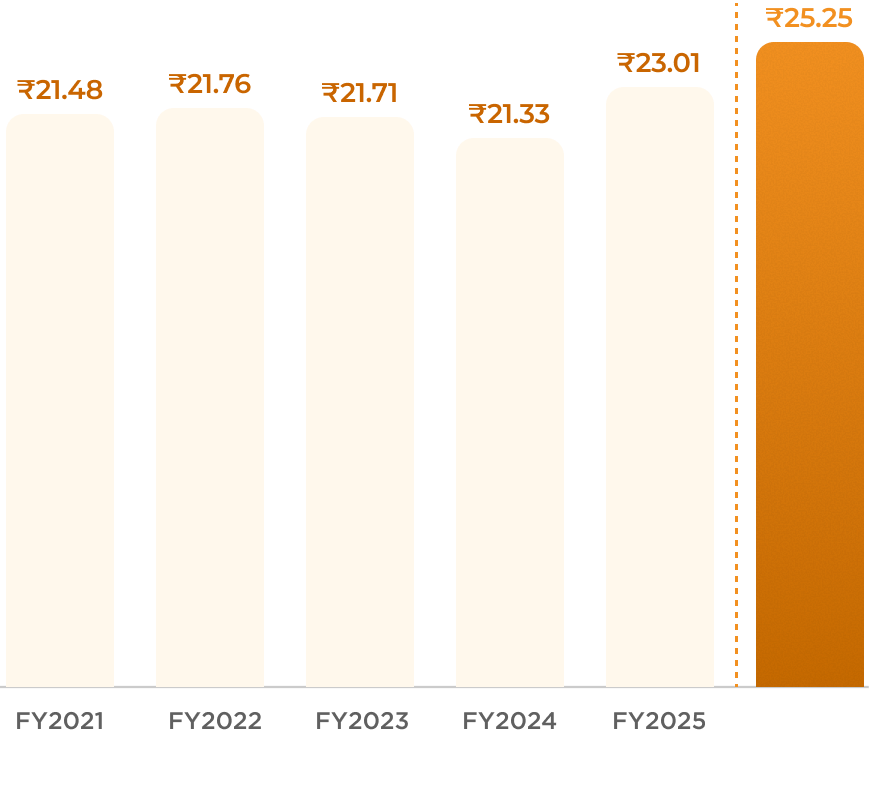

Since listing in April 2019, Embassy REIT has distributed over ₹13,800 crores, a ~100% distributions payout for 27 straight quarters.

Total Distributions since Listing

Total Returns in CY25

Distributions Per Unit in last quarter

Distribution Yield on FY26 mid point guidance

Embassy REIT has a public float of 92%, which is well distributed among foreign and domestic institutions and retail investors.

Market Cap

Public Float

Total Investors

Growth in Retail Investor Base

Embassy REIT is India’s first listed REIT and the largest office REIT in Asia by area. It owns and operates a commercial office portfolio across 5 major cities in India.

Total Area

Office Parks

Gateway Cities

Blue Chip Occupiers

Since listing in April 2019, Embassy REIT has distributed over ₹13,800 crores, a ~100% distributions payout for 27 straight quarters.

Total Distributions since Listing

Total Returns in CY25

Distributions Per Unit in last quarter

Distribution Yield on FY26 mid point guidance

Embassy REIT has a public float of 92%, which is well distributed among foreign and domestic institutions and retail investors.

Market Cap

Public Float

Total Investors

Growth in Retail Investor Base

REIT distributions are tax-efficient, with a significant proportion tax free for investors.

Exempt(1)

Taxable at applicable tax rates.(2)

Reduced from Acquisition Cost(3)

Taxable(4)

(1) There is no further tax on dividends in the hands of the unitholders, as the SPVs of the REIT have not opted for the beneficial corporate tax rate regime.

(2) Withholding tax deducted by the REIT (Non-residents - 5%, Others – 10%)

(3) Not taxable upon receipt, however such proceeds need to be reduced from the cost of acquisition of the units

(4) Assuming on-market sale - LTCG at 12.5% (for holding period >1 year) or STCG at 20%, subject to taxability under applicable DTAA for non-residents.

Website Link

Visit Our WebsiteSocial Links

© 2026 Embassy Group, All Rights Reserved.

Bengaluru (75%)

Mumbai (9%)

Pune (7%)

NCR (6%)

Chennai (3%)

Bengaluru (75%)

Mumbai (9%)

Pune (7%)

NCR (6%)

Chennai (3%)

Total Area: 16.6 msf

Total Area: 9.7 msf

Total Area: 3.1 msf

Total Area: 0.3 msf

Total Area: 1.4 msf

Total Keys: 619 Keys

Total Keys: 247 Keys

Total Keys: 230 Keys

Total Area: 0.5 msf

Total Area: 0.4 msf

Total Area: 1.2 msf

Total Area: 5.5 msf

Total Area: 1.5 msf

Total area: 1.9 msf

Total Area: 3.3 msf

Total area: 1.4 msf

Total area: 5.0 msf

Distributions (₹/Unit)

(1) Guidance for FY2026 is based on our current view of existing market conditions and certain key assumptions for the year ending March 31, 2026. This does not include the impact of any fresh issue of units by the Embassy REIT. Guidance is not reviewed or audited or based on GAAP, Ind AS or any other internationally accepted accounting principles and should not be considered as an alternative to the historical financial results or other indicators of the Embassy REIT's financial performance based on Ind AS or any GAAP. There can be no assurance that actual amounts will not be materially higher or lower than these expectations. In particular, there are significant risks and uncertainties related to the scope, severity and duration of the global macro-economic conditions and the direct and indirect economic effects of the same on the Embassy REIT, our assets and on our occupiers.

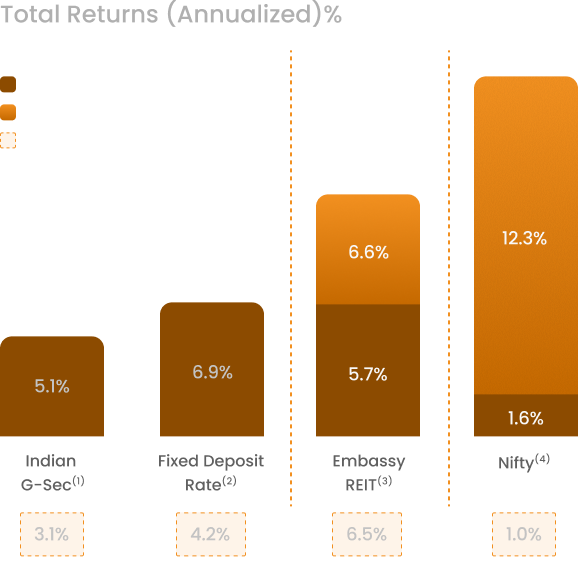

Total Returns (Annualized)%

1) Refers to the Indian 5-year G-Sec yield on December 31, 2020

2) Refers to SBI bank domestic term deposit rate for 5-10 years (for less than ₹2 crores) as on April 01, 2019

3) Performance is calculated basis XIRR. Distribution yield and capital appreciation computed 2019, total distributions paid out since listing on April 01, 2019, IPO price of ₹300 and NSE closing price as of December 31, 2025. Post tax distribution yield is calculated assuming 39% tax rate and interest component of the distribution which is taxable (considering H1 FY2026 distribution split where interest component is 7%)

(4)Nifty – Annualized returns since Embassy REIT listing on April 01, 2019 to December 31, 2025

(5)Tax rate of 39% (Maximum Marginal Tax Rate) considered for calculating all post tax distribution yields

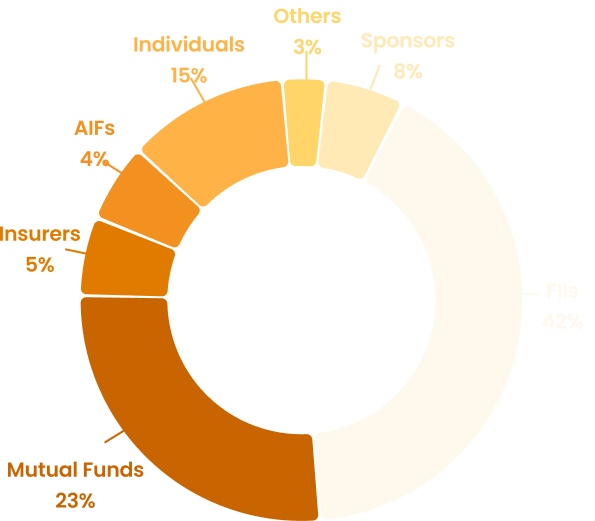

Sponsors - 8%

Public Float - 92%

Capital Group, Bain Capital, The Vanguard Group, BlackRock, JP Morgan AM, Carmignac

ICICI Prudential Mutual Fund, HDFC Mutual Fund, SBI Mutual Fund

Kotak Real Estate Fund

Participation in professionally managed real assets

Easy entry and exit in real estate through buying and selling on stock exchanges

Strong governance framework & disclosure requirements

90% minimum cash flows to be distributed

Potential for capital appreciation

Investment in a diversified portfolio across sectors & cities

Listed Indian REITs

(4 Office, 1 Retail)

Area Across India’s Top Commercial Real Estate Markets

Total Market Capitalization(1)

Total Distributions

Included in multiple equity indices

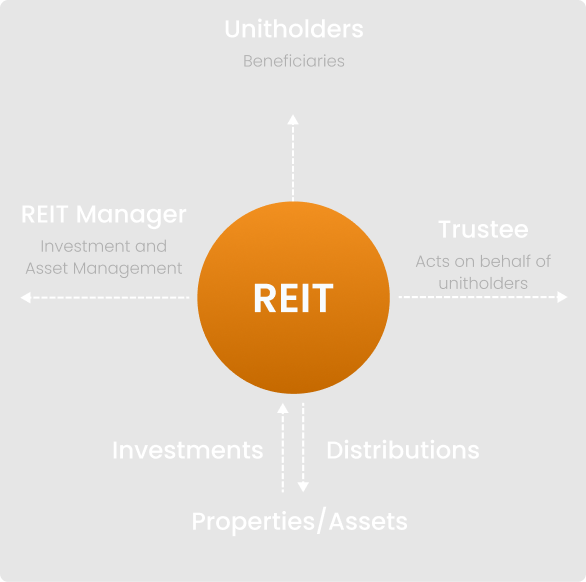

Unitholders

(1)Market Capitalization of Indian REITs basis NSE Closing price on Dec 31, 2025

REIT 101 - Video Library

REIT 101 - Video Library

REIT Primer

REIT Primer

REIT FAQs

REIT FAQs

In the News

In the News

Investor Charter

Investor Charter

+91 80 6935 4864

+91 80 6935 4864  ir@embassyofficeparks.com

ir@embassyofficeparks.com