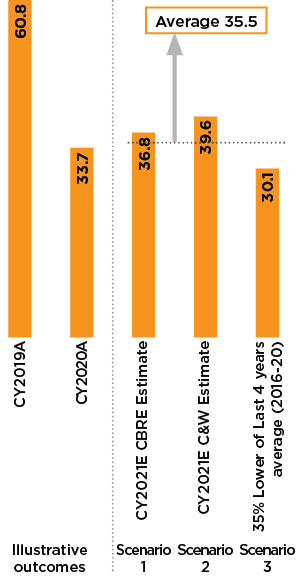

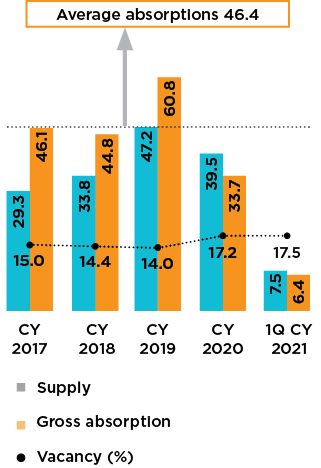

Absorption trends (CY2017 - to date) (msf)

Source: CBRE Research, Embassy REIT

1Q CY2021 highlights

- Leasing momentum slowed down to 6.4 msf in Q1 CY2021, 30% lower than previous quarter

(i) Occupier sentiment impacted with resurgence in COVID-19 cases across all major cities

(ii) Occupiers continued to pause new deals unless driven by immediate business needs - Bengaluru and the technology sector were major demand drivers, contributed to 45% and 35%, respectively of pan‑India absorption

- Despite the resilience, timing of real estate plans to be impacted by the second wave related uncertainty