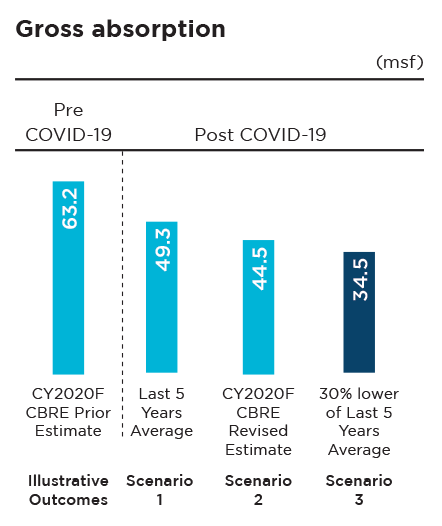

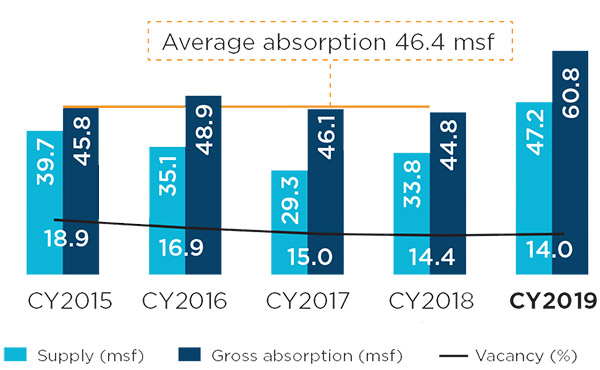

CY2019 was a record year for the Indian office market with c.61 msf of gross absorption. Embassy REIT’s markets witnessed strong fundamentals resulting in record absorption and low vacancy levels.

Absorption trends

- Absorption: Record absorption for Indian

commercial office space in CY2019, c.31%1

higher compared to historical average

- Bengaluru, REIT’s dominant market, continued as India’s leading market with c.30%1 share of historical annual leasing

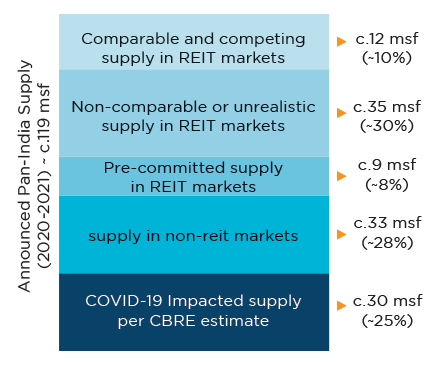

- Supply: Significant pre-commitments witnessed in CY2019 supply of c.47 msf, c.37% y-o-y supply growth average

- Vacancy: Declined c.500 bps to c.14% in the

past five years, primarily driven by technology

sector demand

- Core REIT markets of Bengaluru and Pune witnessed sub-6% vacancy levels

City-wise performance – CY2019

City

Absorption2

(msf) Supply

(msf) Vacancy

(%) Bengaluru 16.1 10.8 4.1 Pune 7.0 4.5 5.6 Mumbai 7.1 4.3 21.0 NCR 11.1 10.5 23.4 Embassy REIT markets 41.3 30.1 13.8 Hyderabad 12.9 13.5 10.4 Chennai 5.5 3.3 8.5 Kolkata 1.1 0.2 36.7 Other markets 19.5 17.1 14.6 Grand Total 60.8 47.2 14.0

(msf) Supply

(msf) Vacancy

(%) Bengaluru 16.1 10.8 4.1 Pune 7.0 4.5 5.6 Mumbai 7.1 4.3 21.0 NCR 11.1 10.5 23.4 Embassy REIT markets 41.3 30.1 13.8 Hyderabad 12.9 13.5 10.4 Chennai 5.5 3.3 8.5 Kolkata 1.1 0.2 36.7 Other markets 19.5 17.1 14.6 Grand Total 60.8 47.2 14.0

Source: CBRE Research, Embassy REIT

Notes:

1 Based on average annual gross absorption from CY2015 to CY2018

2 Represents gross absorption figures